This month, I sold half my Indian equity mutual funds and was researching funds to invest in. I was looking for something safe & long term.

As I was exploring 10-year Gilt Funds (mutual funds that invest in the Indian Government’s 10-year bond), I noticed that they had a pretty high yield — mostly over 10%.

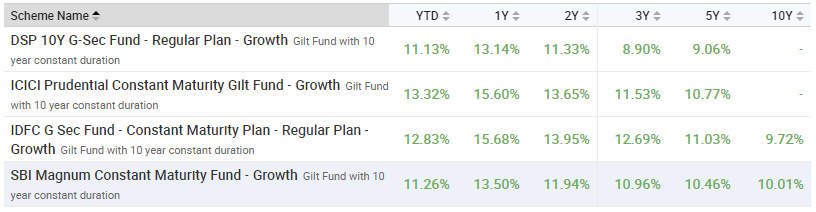

I took a closer look at ICICI Prudential’s Constant Maturity Gilt Fund. (They had the lowest expense ratio.) The annualized returns over the last 5 years were 10.77%, and it’s never fallen below 10% in the last 5 years.

But the strange thing is that the underlying 10-year bond always yielded less than 10% in the last 10 years.

So, how does a mutual fund that buys only one bond yield more than that bond’s ever done in the last 10 years?

(I went ahead and invested. But this is going to worry me to no end.)

Hi Anand: I have been reading your posts for several years now. To help you understand the conundrum,

A constant maturity fund mixes gilts of different longer-term maturities such that the average portfolio maturity stays at 10 years. This strategy has two key benefits. The first and obvious is the absence of credit risk. By investing purely in gilt securities, these funds are less risky than even high-credit-quality debt funds. For instance, an event such as the IL&FS catastrophe can hurt such high-quality debt funds, but will still leave gilt funds unharmed.

The second benefit is that there are no risks of wrong duration calls. Gilt funds, unlike constant maturity funds, will change their portfolio maturities based on the stage of the interest rate cycle. That is, they may go for short-term gilts, or medium-term or even very long-term 20+ years of gilt papers. Dynamic bond funds similarly switch between duration and accrual-based on the direction of the interest rate cycle.

This introduces uncertainty in how well they can capture market opportunities. A dynamic duration strategy needs to get its calls correctly in order to book profits made from bond price rallies. Missteps here can hurt returns. Since constant maturity funds stick to a specific duration, this risk significantly reduces. The strict maturity also ensures that the fund can book and realize the gains made on price appreciation. As an investor, therefore, you get both the accumulated coupon and capital appreciation.

Constant maturity funds have the ability to beat other debt fund categories such as a corporate bond, medium duration, medium to long duration, and other gilt funds especially over a period where interest rates are overall trending lower.

Consider the 5-year rolling return for the period between 2011 to date, of the Nifty 10-year Benchmark G-Sec. While most debt funds from categories such as a corporate bond, dynamic bond, short duration, and medium duration beat the benchmark return, just about half were able to do so more than 60% of the time. That is, the 10-year benchmark G-Sec index was able to beat funds with a good degree of consistency.

Constant maturity funds do not have too long a history. However, their 5-year returns in the past six-year period have beaten funds across debt categories. It is noteworthy that rate cycles have not only become shorter in the past 6 years but have also turned trickier to forecast and manage. This makes constant maturity a strategy devoid of the uncertainties of all other duration categories.

Do remember these funds do not stick only to 10-year papers, but mixes different long-term maturities of 8-13 years such that the overall average maturity remains around 10 years.

Thanks, Ashwin — that was helpful. I researched this specific fund, and it looks like they only invest in the 10-year GoI Gilt fund. But obviously, the time of investment would have varied. Given that interest rates have been generally declining that may explain part of the rise in this fund as well.